Anti-Money Laundering (AML) Policy

Money laundering is the process of concealing illegally obtained funds to make them appear legitimate. Criminals often use a series of complex transactions or international transfers to disguise the source of the money.

Share

Introduction

Money laundering is a serious issue that impacts economies, businesses, and security on a global scale. The United Nations Office on Drugs and Crime estimates that between 2-5% of global GDP—roughly $800 billion to $2 trillion annually—is laundered through illegal channels. This vast flow of illicit money can destabilize financial institutions, promote corruption, and facilitate criminal activities. In response, various laws have been implemented to combat money laundering.

The U.S. Bank Secrecy Act (BSA) mandates that financial institutions monitor and report suspicious activities. At the same time, the European Union’s Anti-Money Laundering Directive (AMLD) requires comprehensive measures to detect and prevent money laundering across EU member states.

An effective Anti-Money Laundering (AML) policy is essential for businesses to protect themselves from these risks and comply with international regulations. If you’re unsure where to start, we’ve outlined the key steps to help you create an AML policy. Alternatively, you can get started by downloading VComply’s Free Downloadable Anti-Money Laundering (AML) Policy Template.

What is Money Laundering?

Money laundering is the process of concealing illegally obtained funds to make them appear legitimate. Criminals often use a series of complex transactions or international transfers to disguise the source of the money. This poses serious risks, as it can facilitate criminal activities such as fraud, terrorism financing, and corruption.

Anti-Money Laundering (AML) policies are essential for organizations to detect and prevent such illicit activities, ensuring compliance with legal requirements and protecting the integrity of the financial system. According to Nasdaq’s report, in 2023 alone, over 3 trillion dollars in illicit funds flowed through the global economy. Effective AML measures help safeguard an organization’s reputation, avoid penalties, and maintain trust among stakeholders and regulators. For those looking to implement robust protections, a Free Downloadable Anti-Money Laundering (AML) Policy Template can be a valuable resource.

Stages of Money Laundering

Money laundering is the deliberate attempt to make illicit funds appear legitimate. Criminals use various techniques to disguise the origins of these funds, and organizations play a critical role in preventing this process through effective Anti-Money Laundering (AML) policies. These policies are essential for ensuring compliance with regulations and mitigating the risks associated with illegal financial activities. Money laundering typically occurs in three stages: placement, layering, and integration.

Placement

The first stage is placement, where illicit money is introduced into the financial system. Criminals often use techniques such as depositing large sums of cash, purchasing high-value assets, or making multiple smaller deposits to avoid detection. The goal of placement is to move the funds away from their criminal origins without raising suspicion, thereby initiating the money laundering process.

Layering

After placement, criminals move to the layer, where the objective is to obscure the money trail. This involves complex transactions such as transferring funds between various accounts, sometimes across borders or converting the money into assets like stocks, bonds, or real estate. By using these techniques, criminals attempt to distance the funds from their illegal origin, making them harder to trace.

Integration

In the final stage, integration, laundered money is reintroduced into the legitimate economy. This can involve investing in businesses, real estate, or other assets, which allows criminals to make the illicit money appear as though it has been obtained through legal means. Once integrated, it becomes difficult to distinguish the laundered money from lawful earnings.

An effective Anti-Money Laundering (AML) framework is essential for identifying and preventing these activities. By implementing robust monitoring systems, conducting thorough due diligence, and adhering to relevant regulations, organizations can significantly reduce the risk of being involved in money laundering operations.

Why do We Need Anti-money Laundering Policies?

Anti-Money Laundering (AML) policies are essential for preventing financial crimes such as fraud, terrorism financing, and corruption. These policies help ensure compliance with global AML regulations and protect institutions from legal and reputational risks. By enforcing robust AML compliance, organizations can safeguard the integrity of the financial system and maintain public trust.

Compliance with Legal Requirements

Organizations are legally obligated to follow AML regulations set by governments and international bodies. Non-compliance can lead to hefty fines, penalties, and even the loss of operating licenses. Strong AML compliance ensures that entities meet regulatory standards and avoid legal repercussions.

Prevention of Financial Crimes

Money laundering is often connected to other forms of criminal activity, such as fraud, corruption, and terrorism financing. By enforcing AML policies, institutions can detect suspicious transactions early and prevent the flow of illicit funds through the financial system, helping reduce organized crime.

Safeguarding Reputation

An organization’s reputation is a key asset, and involvement in money laundering can seriously damage public trust. Implementing effective AML policies and conducting regular monitoring ensures that institutions remain free from associations with criminal activities, preserving their credibility and trust in the market.

Protecting the Integrity of the Financial System

The integrity of the financial system relies on trust and transparency. AML compliance helps preserve this by preventing the illegal movement of money, which can distort markets and harm legitimate businesses. This ensures the stability of financial ecosystems globally.

Minimizing Financial and Legal Risks

Without a solid AML framework, organizations may unknowingly facilitate illicit transactions, exposing them to significant financial and legal risks. Strong prevention measures—such as monitoring transactions, conducting due diligence, and reporting suspicious activities—help mitigate these risks and ensure compliance with legal standards.

Global Financial Cooperation

With financial markets being interconnected globally, countries and regulatory bodies cooperate to combat money laundering. Organizations must follow international AML regulations to ensure consistency, align with global standards, and foster smoother cross-border transactions, maintaining the flow of legitimate funds.

Customer Trust and Confidence

Customers expect institutions to be secure and transparent in their financial dealings. By implementing and adhering to AML policies, organizations reassure their clients that their money is safe and that they are actively working to prevent illegal activities, thereby maintaining customer trust.

Avoiding Sanctions and Penalties

Many organizations have faced severe sanctions due to failing to implement effective AML compliance programs. These penalties can result in reputational harm, loss of business, and operational disruption. Strong AML policies are crucial to avoiding these risks.

Effective AML policies help organizations mitigate risks, comply with regulations, and protect both their reputation and the broader financial system. By prioritizing money laundering prevention, entities safeguard themselves and contribute to a safer and more secure global financial system.

Benefits of Implementing anti-money laundering policy

Implementing an effective Anti-Money Laundering (AML) policy is crucial for organizations aiming to ensure legal compliance, maintain a strong reputation, and safeguard their financial systems. AML policies not only help prevent financial crimes but also foster a secure and professional environment for both employers and employees. Below is a breakdown of the key benefits for employers and employees:

Key Elements of an Anti-Money Laundering (AML) Policy

An Anti-Money Laundering (AML) policy is essential for organizations to ensure compliance with regulations designed to prevent illegal financial activities such as money laundering and terrorist financing. These policies help identify, detect, and prevent suspicious transactions that could involve illicit funds. Below is a breakdown of the key elements that form a well-structured AML policy:

1. Purpose and Scope of the AML Policy

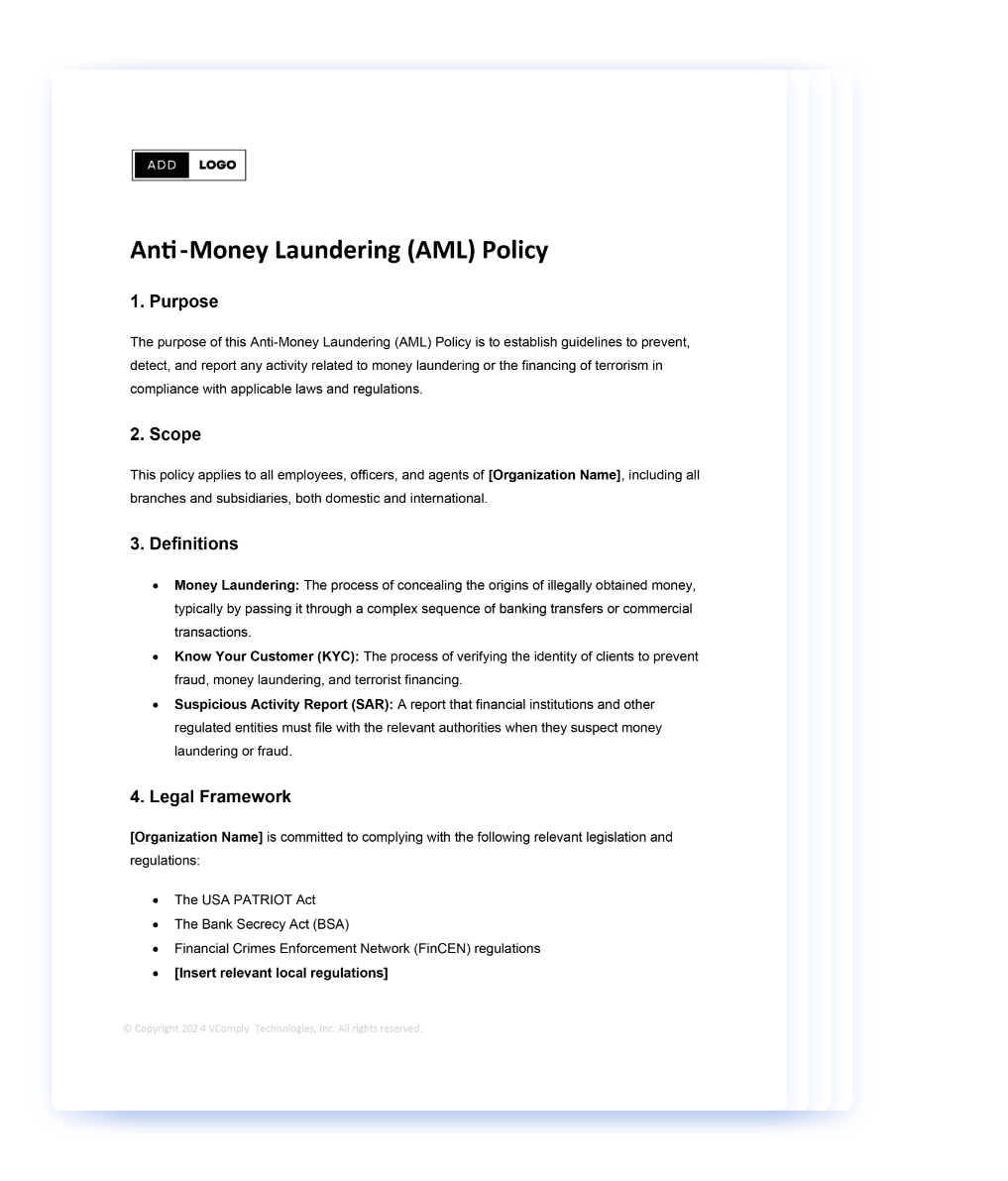

The purpose of this Anti-Money Laundering (AML) Policy is to establish guidelines to prevent, detect, and report any activity related to money laundering or the financing of terrorism in compliance with applicable laws and regulations.

The policy outlines procedures to help identify, detect, and prevent suspicious activities and ensures compliance with both local and international regulations. It is a crucial tool for promoting integrity and transparency within the financial system.

This policy applies to all employees, officers, and agents of [Organization Name], including all branches and subsidiaries, both domestic and international. The policy applies to all employees, departments, and business activities within the organization that interact with financial transactions, client relationships, or regulatory authorities.

2. Transaction Monitoring and Reporting

An effective AML policy includes mechanisms to monitor transactions for signs of suspicious activity continuously. This ensures that the organization can detect potential money laundering activities in real-time and take appropriate action.

- Suspicious Activity Identification: Identify and flag transactions that appear out of the ordinary, such as large, unexplained cash deposits or transfers to or from high-risk countries. This may also include transactions that deviate from a customer’s normal transaction behavior.

- Automated Systems: Utilize advanced software tools to detect unusual transaction patterns based on pre-defined criteria automatically. These systems can help identify transactions that may require additional scrutiny and manual review.

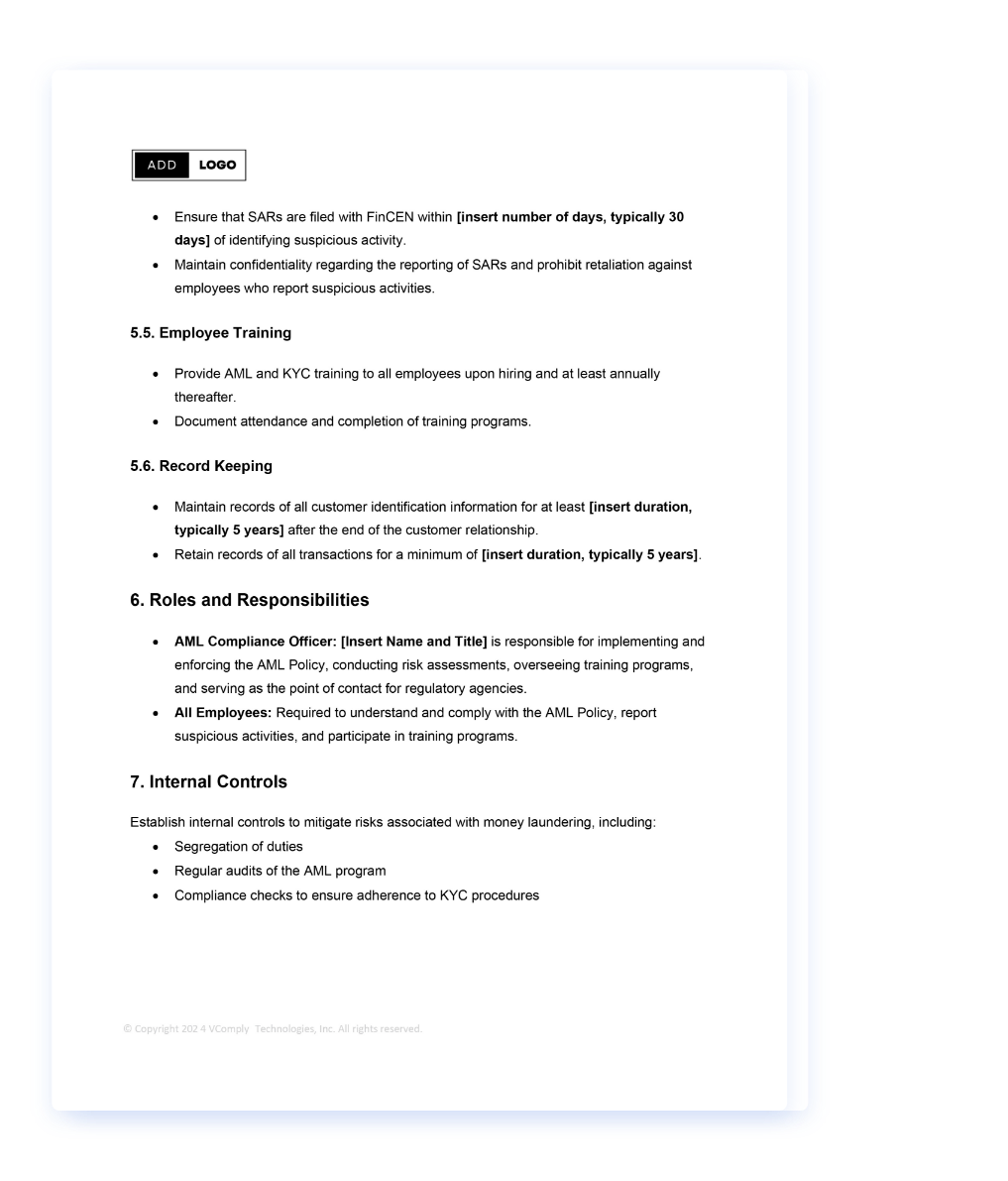

- Suspicious Activity Reports (SARs): When suspicious activity is detected, the organization is obligated to file SARs with the relevant regulatory authorities, such as the Financial Crimes Enforcement Network (FinCEN), within a specified timeframe (typically 30 days). The SAR should include details of the suspicious transaction and the reasons for suspicion.

3. Sanctions Screening

Ensuring compliance with sanctions regulations is crucial to prevent the organization from engaging with individuals or entities involved in illegal or illicit activities. This process includes:

- Screening Against Sanctions Lists: Regularly check customers and transactions against national and international sanctions lists, including those from the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC), the United Nations, or the European Union.

- Freezing Assets: If a customer or transaction is flagged on these lists, the organization must freeze any assets or transactions linked to the individual or entity until further investigation is conducted.

4. AML Compliance Program

A comprehensive AML Compliance Program ensures the organization complies with applicable regulations and effectively prevents financial crimes. The program typically includes the following components:

4.1 Risk Assessment

- Conduct annual risk assessments to identify potential money laundering risks associated with the organization’s products, services, customers, and geographic locations.

- Maintain documentation of risk assessment results and updates.

4.2 Customer Due Diligence (CDD)

Customer Due Diligence (CDD) procedures ensure that the organization properly identifies clients and understands the nature of their business relationships. Key components of CDD include:

- Identity Verification: Collect and verify customer information such as government-issued identification, proof of address, and tax identification numbers.

- Risk Profiling: Assess the potential risks a customer may pose by evaluating factors such as geographic location, transaction history, and business activities. Higher-risk clients should undergo enhanced scrutiny.

- Ongoing Monitoring: Continuously review customer transactions and behavior to identify patterns that deviate from expected norms or raise red flags.

4.3 Know Your Customer (KYC)

KYC procedures are integral to CDD, involving the collection of detailed information about customers to verify their identities and evaluate the legitimacy of their financial activities. Key KYC procedures include:

- Basic Identity Information: Collect basic details such as full name, address, date of birth, nationality, and tax identification number.

- Source of Funds: Understand the origin of a customer’s funds to ensure they are not derived from illegal sources.

- Enhanced Due Diligence (EDD): For high-risk customers, such as politically exposed persons (PEPs) or those from high-risk jurisdictions, conduct a more thorough review, including monitoring their financial transactions more closely.

4.4 Enhanced Due Diligence (EDD) for High-Risk Customers

- EDD Procedures: High-risk customers, including PEPs, individuals from jurisdictions with high levels of financial crime, or customers with complex financial profiles, require enhanced due diligence. This includes obtaining more detailed background information, monitoring transactions closely, and involving legal or compliance experts when necessary.

4.5 Ongoing Monitoring

- Establish systems to monitor transactions for unusual or suspicious activity.

- Define parameters for monitoring, including:

- Transaction size

- Geographic location

- Type of transaction

Implement automated systems to flag suspicious transactions for review.

5. Employee Training

To effectively combat money laundering, employees must be trained to detect and report suspicious activities:

- Employee Training Programs: Provide AML and KYC training to all employees upon hiring and at least annually thereafter.

- Documentation of Training: Document attendance and completion of training programs.

6. Record Keeping

Organizations are required to maintain detailed records for regulatory compliance and to facilitate audits or investigations:

- Customer Identification Records: Maintain records of all customer identification information for at least [insert duration, typically 5 years] after the end of the customer relationship.

- Transaction Records: Retain records of all transactions for a minimum of [insert duration, typically 5 years].

7. Internal Controls and Governance

Robust internal controls and governance mechanisms ensure that the AML policy is properly implemented:

- AML Compliance Officer: Appoint an AML Compliance Officer responsible for overseeing the implementation of the policy, conducting risk assessments, and liaising with regulators.

- Internal Audits and Independent Reviews: Regularly audit the AML program and conduct independent reviews to assess its effectiveness and ensure it remains compliant with changing regulations.

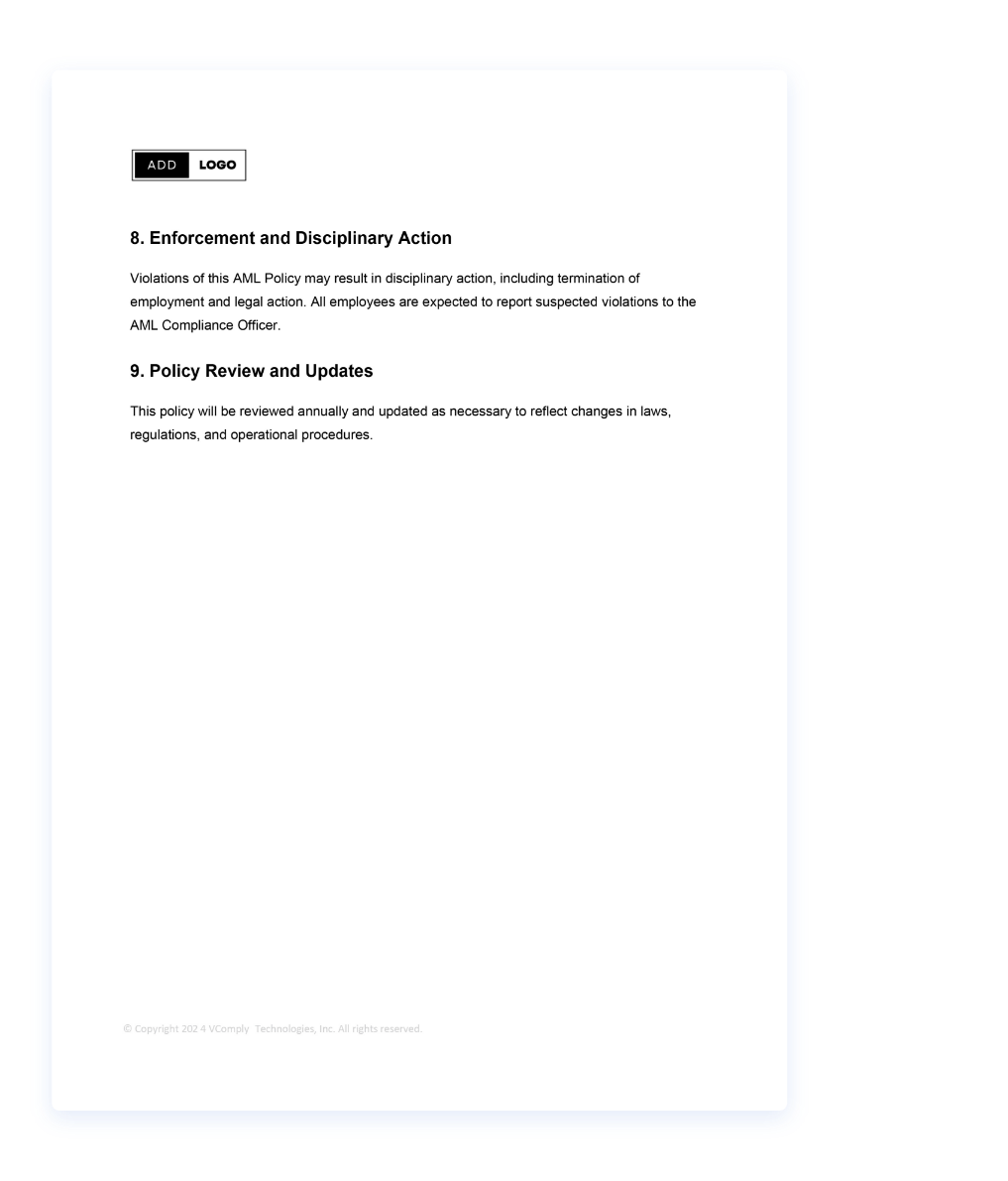

8. Enforcement and Disciplinary Actions

Violations of this AML Policy may result in disciplinary action, including termination of employment and legal action. All employees are expected to report suspected violations to the AML Compliance Officer.

- Disciplinary Measures: Clearly outline the potential consequences for violations of the policy, ranging from internal disciplinary actions to termination and legal penalties.

- Whistleblower Protections: Protect employees who report violations from retaliation, fostering a culture of compliance.

9. Policy Review and Updates

Given the evolving nature of AML regulations and financial crime trends, the policy should be regularly reviewed and updated:

- Annual Reviews: Conduct an annual review to ensure the policy remains compliant with current laws and regulations.

- Regulatory Updates: Modify the policy as necessary to align with new laws, regulations, or international standards.

10. Legal Framework

A strong legal foundation ensures the organization’s AML policy aligns with local and international regulatory standards:

For example, [Organization Name] is committed to complying with the following relevant legislation and regulations:

- The USA PATRIOT Act

- The Bank Secrecy Act (BSA)

- Financial Crimes Enforcement Network (FinCEN) regulations

- [Insert relevant local regulations]

A well-structured AML policy is crucial for mitigating the risks of financial crimes. By implementing comprehensive procedures for customer verification, transaction monitoring, reporting, and compliance, organizations can protect themselves from being used for illicit financial activities. For those seeking to streamline the process, a Free Downloadable Anti-Money Laundering (AML) Policy Template can serve as a useful starting point. Regular training, strong internal controls, and a clear governance structure are fundamental to the success of any AML program.

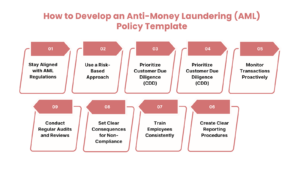

How to Develop an Anti-Money Laundering (AML) Policy Template

Creating a solid Anti-Money Laundering (AML) policy goes beyond just legal requirements; it’s about protecting your institution from financial crimes and ensuring long-term stability. Here’s a straightforward guide to help you build an AML framework that’s both compliant and effective.

Stay Aligned with AML Regulations

The first step in creating your AML policy is understanding the regulations that apply to your organization. These include national laws, international standards like FATF recommendations, and industry-specific rules. Your policy must reflect these legal requirements, and it should be reviewed regularly to stay current as regulations evolve.

Use a Risk-Based Approach

Money laundering risks vary significantly across sectors. By applying a risk-based approach, you can identify where the greatest threats lie—whether that’s in certain customer profiles, geographic areas, or types of transactions. This allows you to allocate resources where they are most needed rather than adopting a one-size-fits-all approach.

Prioritize Customer Due Diligence (CDD)

An effective AML policy focuses on understanding your customers—Customer Due Diligence (CDD) is key. For higher-risk individuals or entities, apply Enhanced Due Diligence (EDD), conducting more detailed background checks and ongoing monitoring. The goal is to understand who you’re dealing with and identify any potential red flags early.

Monitor Transactions Proactively

Automated monitoring systems are critical for flagging suspicious activities. These systems should be capable of detecting irregular patterns, whether it’s an unusual series of payments or cross-border transactions. The objective is to catch any signs of money laundering in real-time and ensure immediate intervention if necessary.

Create Clear Reporting Procedures

Your AML policy must outline the steps for reporting suspicious transactions. Ensure that employees or relevant parties have a secure and straightforward process for flagging issues internally. Suspicious Activity Reports (SARs) should be filed promptly with the relevant authorities. Clear reporting protocols minimize the chances of missing potential red flags.

Train Employees Consistently

Employees are your first line of defense against money laundering. Regular training sessions should cover identifying suspicious behavior, understanding how money laundering works, and the legal consequences of non-compliance. The more well-prepared your team is, the better your chances of detecting illicit activity early.

Set Clear Consequences for Non-Compliance

Make it clear that failing to follow AML procedures will not be tolerated. The policy should outline specific consequences for non-compliance, whether that involves disciplinary action or legal ramifications for the organization. This helps establish a culture of accountability.

Conduct Regular Audits and Reviews

An AML policy should not be static. Regular internal audits and reviews are essential to assess how effectively your policy is being implemented and to identify any gaps. You should also adjust the policy if there are significant changes in your operations, the regulatory environment, or emerging threats.

Create a Continuous Improvement Process

The fight against money laundering is ongoing, and your AML framework should reflect that. Establish a process for continuous improvement, where feedback is gathered, systems are updated, and new risks are addressed. Money laundering techniques evolve, and so should your defenses.

By following these steps, you can create an AML policy that not only ensures compliance with relevant regulations but also serves as a proactive defense against money laundering activities. The goal is to establish a flexible, responsive system that effectively safeguards your organization.

Get started on building a solid Anti-Money Laundering (AML) policy for your organization with VComply’s free downloadable AML policy template. This easy-to-use template will help you establish the necessary controls and ensure compliance with regulatory requirements.

FAQs

1. What is an anti-money laundering policy?

An Anti-Money Laundering (AML) policy is a set of procedures, laws, and regulations designed to prevent illegal activities such as money laundering and terrorist financing. This policy requires businesses to monitor transactions, verify customer identities, and report suspicious activities to regulatory authorities.

2. Why do we need anti-money laundering policies?

AML policies are essential for money laundering prevention and safeguarding the financial system. They help businesses detect and prevent illegal activities, protect against financial crimes, and ensure compliance with regulations such as the Bank Secrecy Act (BSA) and the USA PATRIOT Act. Effective AML compliance also protects the organization’s reputation and reduces the risk of legal penalties and financial losses.

3. What are the key elements of an anti-money laundering policy?

A well-structured AML policy includes the following key elements:

- Customer Due Diligence (CDD): Verifying the identity of customers to assess risk.

- Transaction Monitoring: Monitoring transactions for suspicious activity.

- Suspicious Activity Reporting (SAR): Reporting suspicious transactions to regulatory authorities.

- Record Keeping: Keeping accurate records of transactions and customer identification for a defined period.

- Employee Training: Educating staff to recognize and report suspicious behavior.

- Compliance Officer: Appointing an AML compliance officer responsible for enforcing the policy.

4. What type of businesses need an anti-money laundering policy

Businesses that handle financial transactions, particularly those dealing with large sums of money, are required to implement Anti-Money Laundering (AML) policies. This includes credit unions, casinos, real estate agencies, insurance companies, and law firms. Any business within the financial sector, or those dealing with high-value goods or services, must comply with AML regulations to prevent their use in money laundering or terrorist financing activities.

5. What are the 4 pillars of AML policy?

The four pillars of an AML policy are:

- Internal Controls: Establishing processes and systems to monitor and report suspicious activities.

- Compliance Officer: Appoint a designated individual responsible for ensuring compliance with AML regulations.

- Training: Regularly educating employees on the risks of money laundering and how to detect and report suspicious transactions.

- Independent Audit: Conducting periodic audits to assess the effectiveness of the AML program and its compliance with laws.

6. What is the anti-money laundering policy on KYC?

Know Your Customer (KYC) is a key component of an AML policy. It involves the process of verifying the identity of clients to prevent fraud and money laundering. Businesses are required to collect and validate information such as name, address, date of birth, and identification numbers. Enhanced due diligence (EDD) may be required for high-risk customers to assess further their potential involvement in money laundering or terrorist financing.

7. Who is required to have an AML policy?

Any business or financial entity engaged in financial services, transactions, or products must implement an Anti-Money Laundering (AML) policy. This includes insurance companies, law firms, real estate agencies, and even cryptocurrency exchanges. Organizations regulated by the Financial Action Task Force (FATF) or local regulatory authorities are required to develop and maintain AML compliance programs.

8. What is the 6 AML policy?

The 6 AML policy generally refers to six core components of an Anti-Money Laundering policy that include:

- Customer Identification Program (CIP): Verifying customers’ identity.

- Transaction Monitoring: Monitoring for suspicious or unusual transactions.

- Suspicious Activity Reporting (SAR): Reporting any identified suspicious activities to authorities.

- Record Keeping: Maintaining transaction records and KYC documentation.

- Training: Educating staff about AML procedures and recognizing red flags.

- Independent Testing: Conducting internal audits or third-party reviews to evaluate the AML program’s effectiveness.

By integrating these components into a robust AML framework, businesses can enhance their ability to detect and prevent illicit financial activities.

VComply helps simplify Policy creation and maintenance

Our all-in-one solution streamlines drafting, approval, and maintenance processes, providing real-time tracking and seamless collaboration across departments and regions.

Key Features of VComply’s Policy Management:

- Comprehensive Dashboard: Track policy progress from draft to approval in one place.

- Optimized Drafting & Approvals: Collaborate efficiently with clear approval workflows.

- Custom Templates: Use pre-loaded or custom templates for consistency and speed.

- Simplified Attestation: Ensure easy, device-friendly policy attestation for all employees.

- Version Control & Tracked Changes: Keep policies up to date with full version history.

- Approval Workflows: Streamline approval with multi-level workflows.

- Advanced Search & Access Control: Find policy content quickly and control access securely.

- Automation: Automate reminders, reviews, and notifications for better efficiency.

- Integration: Receive policy updates in your favorite tools like Slack or Outlook.

Request a demo today and see how VComply can simplify your policy management.

Final Thoughts

A strong Anti-Money Laundering (AML) policy is essential for organizations, offering much more than just a means to comply with regulations. It acts as a critical shield against financial crime, helping organizations avoid legal, reputational, and operational risks. By focusing on key elements such as Customer Due Diligence (CDD), transaction monitoring, and ongoing employee training, organizations can establish a robust defense against money laundering and terrorist financing activities.

Organizations that take a proactive approach to AML not only remain compliant but also build trust with their stakeholders. This trust is crucial in today’s complex financial landscape, where both internal vigilance and regulatory oversight play key roles in safeguarding the integrity of the financial system.

As money laundering tactics continue to evolve, so too must the policies and strategies designed to counter them. An effective AML policy should be dynamic, regularly updated, and continuously reinforced through training and audits. By doing so, organizations can create a safer environment for their customers, employees, and the financial system at large while minimizing the risks posed by illicit activities.

Check out other policy templates

Information Security Policy

With cyber threats becoming more advanced, businesses must prioritize securing their sensitive data. Information security is no longer optional—it’s a necessity.

Data Retention Policy

By 2024, global data creation is set to hit 149 zettabytes, with projections reaching 394 zettabytes by 2028. As the volume of data grows, managing it efficiently has never been more critical.

Minimum Necessary Rule Policy

When it comes to protecting sensitive data, one of the most important principles to follow is the Minimum Necessary Rule. This rule limits access to only the information necessary to complete a specific task, reducing the risk of unnecessary exposure.

Anti-Money Laundering (AML) Policy Policy

For your own record keeping, we’ll also send a copy of the policy to your email.