Cultivating a Culture of Compliance in Financial Services

In Financial Services Industry, compliance isn’t just a buzzword; it’s the foundation upon which the entire industry stands. The financial services sector is one of the most heavily regulated, and for good reason.

The potential impact of financial misconduct or a breach of trust can be devastating, not only for institutions but for economies and individuals as well. In this blog, we’ll explore the significance of compliance in financial services and the key aspects of staying on the right side of the law.

The Critical Importance of Compliance

The financial services industry is fundamentally built on a foundation of trust. Customers place their valuable finances in the hands of banks, insurance companies, investment firms, and other financial institutions, with the expectation of transparency, ethical behavior, and a dedication to protecting their economic well-being. Compliance stands as the industry’s commitment to upholding this assurance.

Regulatory Landscape: The financial services industry operates under a web of regulations, from anti-money laundering (AML) and know your customer (KYC) rules to the Dodd-Frank Act and Basel Accords. These regulations are designed to protect consumers, ensure market stability, and prevent financial crimes.

Preventing Misconduct: Compliance acts as a safeguard against financial misconduct. Whether it’s insider trading, fraud, or mismanagement, the industry’s adherence to regulatory standards helps maintain trust in the system.

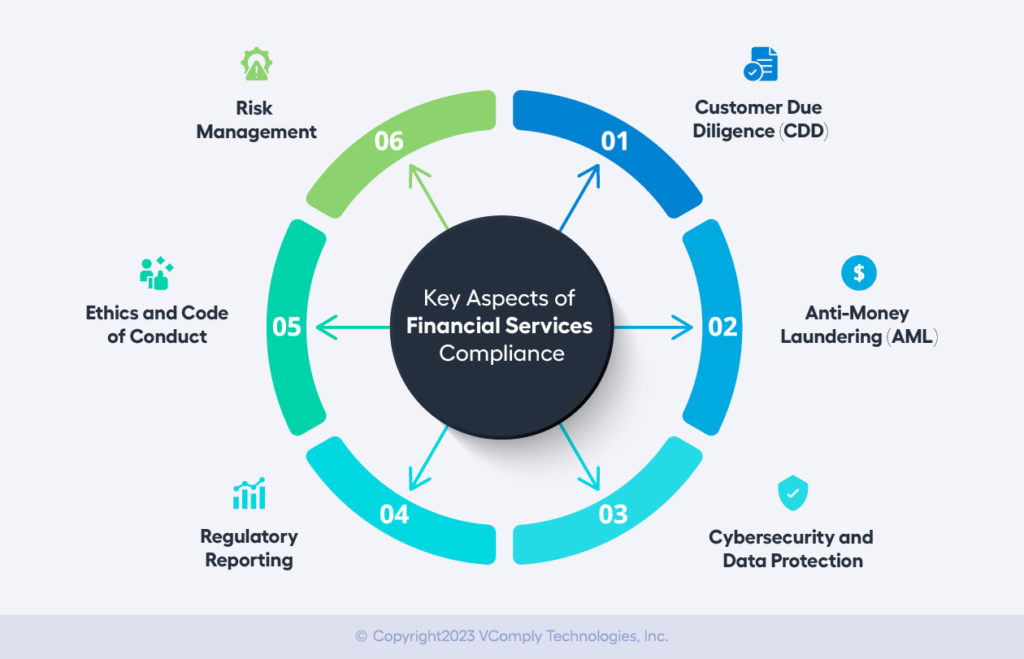

Key Aspects of Financial Services Compliance

Now, let’s dive into some of the fundamental aspects of compliance within the financial services industry:

1. Customer Due Diligence (CDD): Establishing the identity of customers, assessing their risk profiles, and ongoing monitoring are essential to prevent financial crimes such as money laundering and fraud.

2. Anti-Money Laundering (AML): AML measures are in place to detect and prevent money laundering activities. They include transaction monitoring and reporting of suspicious transactions to regulatory authorities.

3. Cybersecurity and Data Protection: With the rise in cyber threats, banks and financial institutions must secure customer data and protect against data breaches. Regulatory bodies now require robust cybersecurity measures to safeguard sensitive information.

4. Regulatory Reporting: Accurate and timely regulatory reporting is crucial. This includes financial disclosures, transaction records, and regulatory filings, all of which must comply with specific standards.

5. Ethics and Code of Conduct: A strong code of ethics and a culture of compliance are critical to ensure employees act with integrity, adhering to the highest ethical standards.

6. Risk Management: Risk management is an ongoing process to identify, assess, and mitigate risks associated with compliance. Regular reviews are essential in a dynamic regulatory environment.

Tackling Compliance Challenges in the Financial Industry

The compliance challenges in the financial sector are addressed through a combination of strategies and best practices:

Regulatory Complexity: Financial regulations are complex and constantly evolving. To tackle this challenge, financial institutions should:

- Stay Informed: Keep abreast of regulatory changes through subscriptions, industry associations, and regulatory agencies’ websites.

- Regulatory Technology (RegTech): Use RegTech solutions that automate compliance processes and provide real-time updates on regulatory changes.

Data Privacy and Security: With increasing concerns about data breaches and cyber threats, it’s essential to protect sensitive customer information. Here’s how to address this challenge:

- Data Encryption: Implement robust data encryption protocols to secure customer data.

Regular Audits: Conduct regular security audits and penetration testing. - Employee Training: Train employees to recognize and prevent data breaches and cyberattacks.

- Anti-Money Laundering (AML) and Know Your Customer (KYC) Regulations: Financial institutions must verify customer identities and report suspicious transactions. To tackle this challenge:

- Automated AML/KYC Processes: Implement automated AML/KYC solutions to streamline the onboarding process.

- Customer Due Diligence: Perform ongoing customer due diligence to monitor transactions and customer behavior.

Cross-Border Regulations: Global financial institutions must navigate different regulatory requirements in various countries. Here are some strategies:

- Local Expertise: Employ compliance experts with knowledge of local regulations in each country you operate.

- Regulatory Mapping: Create a comprehensive regulatory map to track requirements in different jurisdictions.

Promote a culture of Compliance: Leadership Commitment: Ensure that leadership is committed to compliance and sets an example.

- Training and Awareness: Regularly educate employees on compliance requirements and the consequences of non-compliance.

Record-Keeping and Reporting: Maintaining comprehensive records and accurate reporting is essential. To address this:

- Document Management Systems: Implement efficient document management systems to store and retrieve records.

- Automated Reporting Tools: Utilize automated reporting tools to ensure accuracy and timeliness in regulatory reporting.

- Compliance Technology: Leverage technology to address compliance challenges

Third-Party Risk Management: Many financial institutions rely on third-party vendors for various services. To mitigate risks:

- Due Diligence: Conduct thorough due diligence on third-party vendors.

- Contractual Protections: Ensure that contracts with third-party vendors include compliance clauses and expectations.

Audit and Internal Controls: Regular audits and internal controls are essential for identifying and rectifying compliance issues. This involves:

- Internal Auditing: Establish a dedicated internal audit department to review and assess compliance controls.

- Whistleblower Programs: Encourage employees to report compliance violations through confidential whistleblower programs.

Compliance Testing and Monitoring: Implement regular compliance testing and monitoring to ensure that policies and procedures are being followed consistently.

Tackling compliance challenges in the financial services industry requires a proactive and holistic approach, involving technology, people, and processes. It’s essential to adapt to evolving regulations and continuously improve compliance practices to meet industry standards and maintain trust with customers and regulators.

The Role of Technology in Compliance

Technology plays a pivotal role in managing compliance in the financial services sector. Regulatory technology (Regtech) solutions are increasingly used for automating compliance processes, enhancing reporting capabilities, and streamlining risk management.

Technological advancements have become a driving force behind the transformation of compliance processes and procedures in the financial sector. This blog delves into the pivotal role of technology in ensuring compliance and navigating the intricate landscape of the financial services industry.

Enhanced Regulatory Reporting

The financial services industry is governed by an intricate web of regulations and reporting requirements. Technology empowers organizations to streamline these processes, automating the collection, validation, and submission of regulatory reports. Automated regulatory reporting not only reduces the risk of errors but also ensures timely and accurate compliance with regulatory authorities.

Data Analytics for Risk Management

The abundance of data in the financial sector provides a goldmine of insights for risk management and compliance. Advanced data analytics tools allow financial institutions to harness this data to identify potential risks and compliance issues. By leveraging these tools, organizations can proactively manage and mitigate risks, improving their overall compliance posture.

Roadmap to Compliance Automation

As the industry moves toward a more technologically driven future, automating compliance processes has become not just an option but a necessity. In this blog, we’ll outline a strategic roadmap to guide financial institutions in successfully automating their compliance processes.

- Establish Clear Strategies:

Begin your automation journey by setting clear objectives and strategies. Understand the goals you aim to achieve through automation. These could include reducing errors, improving efficiency, enhancing reporting accuracy, and ensuring regulatory adherence.

- Select the Processes to be Automated:

Identify the specific compliance processes and activities that are most suitable for automation. Start with routine and rule-based tasks that can benefit from the precision and consistency of automation.

- Set Priorities:

Not all compliance processes are equal in complexity or risk. Prioritize automation efforts by focusing on critical processes that have the most significant impact on compliance and risk management. This step ensures a strategic and targeted approach.

- Set Governing Structure:

Establish a governance structure that oversees the automation process. Define roles and responsibilities within your organization, including compliance officers, IT experts, and project managers. This ensures accountability and efficient decision-making.

- Select the Technology:

Choose the right technology solutions to support your compliance automation efforts. Compliance management software, artificial intelligence (AI), machine learning, and data analytics tools can all play a vital role in automating processes.

- Select the Implementation Plan:

Craft a comprehensive implementation plan that outlines the steps, timelines, and resources required for each stage of automation. Ensure that your plan is adaptable and can accommodate any changes or roadblocks that may arise.

- Execute the Plan:

Put your carefully designed plan into action. Collaborate with your team to implement the chosen technology solutions, integrate data sources, and initiate automation in compliance processes.

- Monitor and Refine:

Continuous monitoring is essential to ensure that automation is working effectively and compliantly. Periodically review and refine the automated processes, making adjustments as needed.

- Employee Training and Involvement:

Involve your employees in the automation process. Offer training and workshops to help them adapt to the changes. Encourage feedback to identify areas for improvement and enhance the transition process.

Leveraging VComply for Financial Services Compliance

VComply serves as a comprehensive compliance software solution that empowers organizations in numerous critical aspects of compliance management. The platform excels in establishing a robust compliance framework by offering tools for defining roles, assigning responsibilities, and implementing controls. With VComply, tracking compliance activities becomes a streamlined process, ensuring that each task is accounted for and completed on time. This is further reinforced by the assignment of responsibilities to stakeholders, enhancing accountability and transparency across the compliance landscape.

VComply’s versatile workflows facilitate seamless collaboration between departments, while its due diligence scoring and compliance assessment capabilities provide a systematic approach to evaluating adherence to regulations. Risk assessment is made more effective through the platform’s insightful tools, allowing organizations to identify and prioritize potential compliance risks. Document sharing and evidence management become effortless with VComply, enabling easy access to necessary information. The platform’s dashboard reports offer a comprehensive overview of compliance activities, supported by alerts and notifications that keep teams informed in real time. With its multifaceted capabilities, VComply stands as a vital ally in the pursuit of comprehensive compliance management.

Consider implementing VComply to effectively identify and manage potential compliance management challenges, ensuring the compliance and success of your organization in the long run.

Request a demo today to learn more about how VComply can help your business.