How to Conduct an Effective Audit: A Step-by-Step Approach and a Checklist for Success

Internal audits are crucial in promoting transparency, accountability, and effective compliance and governance within organizations. They provide an independent and objective evaluation of a company’s operations, internal controls, and risk management practices.

Audits serve various purposes and are essential for stakeholders such as investors, owners, lenders, and regulatory bodies. The audited reports instill confidence in these parties by validating the accuracy and reliability of the company’s operations and compliance information. This, in turn, helps stakeholders make informed decisions regarding their investments, financial partnerships, or regulatory compliance.

Besides validating compliance records, audits also offer valuable insights into the efficiency and effectiveness of a company’s internal controls, processes, and procedures. Auditors assess the internal control environment to ensure adequate safeguards are in place to mitigate risks, prevent fraud, and maintain the integrity of financial information. Through this assessment, auditors can identify any weaknesses or areas for improvement, providing valuable feedback to management.

Key takeaways (TL;DR)

- Understand how internal audits strengthen governance, compliance, and operational efficiency across organizations.

- Discover the complete audit process—from planning objectives to finalizing reports effectively.

- Learn how structured audit checklists enhance accuracy, transparency, and regulatory compliance.

- Explore how internal audits help identify risks, inefficiencies, and areas for continuous improvement.

- Get insights into how VComply’s Internal Audit Management software streamlines and automates every audit stage.

What is Internal Audit?

Regardless of the geographical location, the audit process involves the meticulous examination and investigation of a company’s processes and records. This can be carried out by experts, or internal auditors who the organization itself employs. The main objective of the audit is to provide an unbiased and expert opinion on the company’s transactions and dealings and provide reports. These reports undergo scrutiny by qualified auditors to ensure they present a true and accurate depiction of the company’s financial position.

To ensure the success and efficiency of internal audits, auditors rely on a well-structured and comprehensive checklist that guides them through the entire audit process.

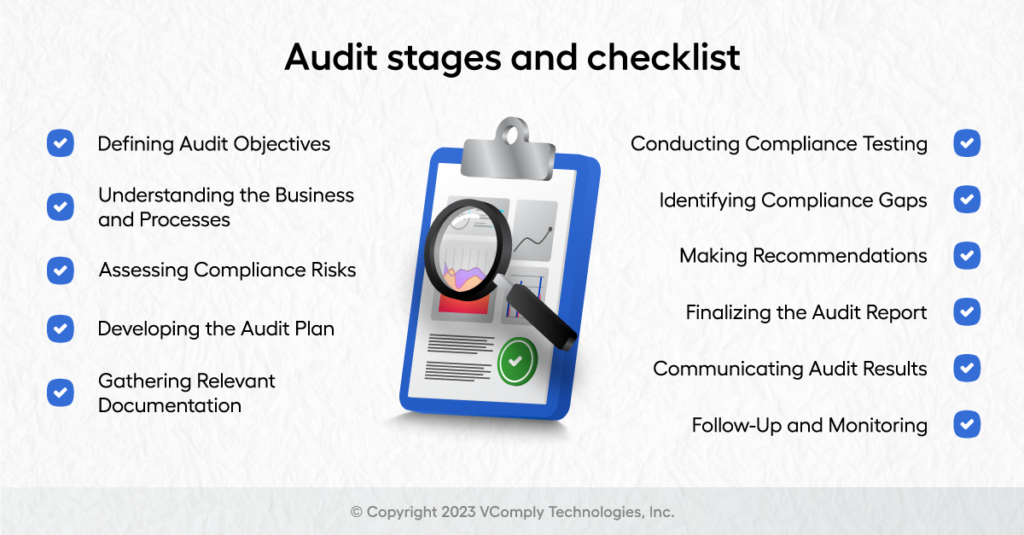

Audit stages and checklist

The stages of the audit planning process are summarized as follows:

Defining Audit Objectives: The first audit planning stage involves clearly defining the compliance objectives. This includes identifying the applicable laws, regulations, and industry standards that the organization must comply with. It also involves understanding the organization’s internal policies and procedures related to compliance.

These objectives should align with the organization’s overall goals and focus on significant risk areas. The checklist should include questions such as:

- What are the specific objectives of the audit?

- Which processes, departments, or functions will be audited?

- Are there any regulatory or compliance requirements that need to be considered?

Understanding the Business and Processes: To conduct a comprehensive audit, auditors must have a deep understanding of the organization’s/project’s operations, processes, and internal controls. The checklist should include items that help auditors gather relevant information, such as:

- Documenting the organization’s structure, including reporting lines and key personnel.

- Identifying the key processes and their interdependencies.

- Reviewing process documentation, policies, and procedures.

- Assessing the organization’s risk management framework.

Assessing Compliance Risks: In this stage, the auditor conducts a comprehensive assessment of compliance risks faced by the organization. This involves identifying potential areas of non-compliance, evaluating the impact and likelihood of risks, and prioritizing them based on their significance. The goal is to focus audit resources on high-risk areas to ensure effective compliance management. An effective internal audit assesses the organization’s risk management practices and identifies areas of improvement. The checklist should include items related to risk assessment and management, such as:

- Evaluating the organization’s risk identification and assessment processes.

- Reviewing risk mitigation strategies and controls.

- Assessing the adequacy of risk monitoring and reporting mechanisms.

- Ensuring risks are regularly reviewed and updated.

Developing the Audit Plan: The auditor develops an audit plan based on the identified compliance objectives and risks. This plan outlines the scope of the audit, the audit procedures to be performed, and the resources required. It also includes a timeline for conducting the audit and completing the necessary documentation.

The checklist should include items such as:

- Define audit methodology and approach.

- Establish audit timelines and resources.

- Determine the appropriate sampling techniques.

- Define the criteria for evaluating compliance and performance.

- Create a detailed plan outlining the audit steps.

- Specify the audit tests and techniques to be employed.

- Assign responsibilities and timelines for each task.

Gathering Relevant Documentation: The auditor requests and gathers relevant documentation related to compliance. This may include policies, procedures, contracts, licenses, permits, training records, incident reports, and other supporting documents. The purpose is to comprehensively understand the organization’s compliance framework and assess its effectiveness.

The checklist should include items such as:

- Policies and procedures.

- Contracts and agreements.

- Internal control documentation, including change management.

- Financial records.

- Employee records.

- Incident and logs.

- Previous audit reports and training materials.

- Correspondence and communication.

Conducting Compliance Testing: In this stage, the auditor performs testing procedures to evaluate the organization’s compliance with applicable laws and regulations. This may involve sample testing, interviews with employees, observation of processes, and review of control activities. The objective is to determine the extent of compliance and identify any instances of non-compliance.

The checklist should include items such as:

- Specify the testing methods and techniques.

- Determine the sample size and selection criteria.

- Review Documentation.

- Conduct Interviews.

- Perform testing procedures.

- Collect evidence.

- Evaluate findings.

Identifying Compliance Gaps: Based on the compliance testing results, the auditor identifies any areas of non-compliance or potential compliance gaps. This includes instances where the organization’s practices deviate from the required standards or where controls are inadequate. The findings are documented for further analysis and discussion with management.

Leveraging data analysis, techniques can enhance the efficiency and effectiveness of internal audits. The checklist should incorporate steps for:

- Gathering relevant data for analysis.

- Conducting data analytics to identify anomalies, trends, or potential areas of concern.

- Using data visualization tools to present findings effectively.

- Identify root causes.

Making Recommendations: The auditor provides recommendations to address the identified compliance gaps and improve the organization’s overall compliance program. These recommendations may include implementing or enhancing control measures, revising policies and procedures, conducting training programs, or engaging external experts for specialized compliance areas. The recommendations aim to strengthen the organization’s compliance posture and mitigate compliance risks.

The checklist should include items related to:

- Understand the audit findings.

- Develop actionable recommendations.

- Consider industry best practices and align them with the organization’s goals.

- Collaborate with stakeholders.

- Develop implementation plan.

Finalizing the Audit Report: The auditor prepares a final audit report that summarizes the findings, recommendations, and overall compliance assessment. The report is shared with management and other relevant stakeholders for review and feedback. It undergoes a thorough review process to ensure accuracy, completeness, and clarity. The checklist should include items related to:

- Recording detailed audit observations and conclusions.

- Identifying control weaknesses, non-compliance issues, or areas of improvement.

- Assigning appropriate risk ratings or severity levels.

- Recommending corrective actions and improvements.

Communicating Audit Results: Effectively communicating audit results is crucial for driving organizational change and improvement. The checklist should include steps for:

- Preparing comprehensive audit reports with clear and concise findings.

- Present audit results to management and stakeholders.

- Facilitating discussions on identified issues and recommended actions.

- Ensuring that corrective actions are tracked and implemented.

Follow-Up and Monitoring: After the audit report is finalized and issued, the auditor may engage in follow-up activities to monitor the implementation of recommendations. This includes tracking management’s actions, assessing the effectiveness of remediation efforts, and providing ongoing support to ensure sustained compliance improvement.

- Review Audit Recommendations.

- Develop Action Plans.

- Allocate Resources.

- Track progress.

- Document changes.

- Continuous improvement.

- Conduct follow-up audits.

By following these stages of audit planning from a compliance perspective, organizations can proactively manage compliance risks, demonstrate their commitment to legal and regulatory requirements, and enhance their overall compliance framework.

Significance of Internal Auditing

Enhancing Internal Controls: Internal audits help organizations strengthen their internal controls. By evaluating the design and effectiveness of control measures, auditors identify potential gaps or weaknesses. This enables management to implement corrective actions and improve the organization’s overall control environment, reducing the risk of fraud, errors, and non-compliance.

Ensuring Compliance: Compliance with laws, regulations, and industry standards is essential for organizations to maintain their reputation and avoid legal and financial consequences. Internal audits assess the organization’s adherence to these requirements, highlighting any areas of non-compliance. Organizations can identify compliance gaps through regular audits and take corrective measures to mitigate risks.

Identifying Operational Inefficiencies: Internal audits provide an opportunity to evaluate operational processes and identify inefficiencies or areas for improvement. By examining workflows, resource allocation, and productivity levels, auditors can recommend enhancements to streamline operations, reduce costs, and improve overall efficiency.

Mitigating Risk: Risk management is a critical aspect of organizational success. Internal audits assess risks faced by the organization, including financial, operational, strategic, and compliance risks. By identifying and evaluating risks, auditors assist management in developing appropriate risk mitigation strategies and controls. This proactive approach helps prevent potential losses and safeguard the organization’s assets.

Safeguarding Assets: Internal audits focus on safeguarding the organization’s assets, including physical assets, intellectual property, and sensitive information. By assessing the adequacy of security measures, access controls, and data protection practices, auditors help protect the organization’s valuable resources from theft, unauthorized access, or misuse.

Improving Financial Reporting: Accurate and reliable financial reporting is essential for stakeholders to make informed decisions. Internal audits examine financial processes, transactions, and reporting systems to ensure compliance with accounting standards and the accuracy of financial statements. By verifying the integrity of financial information, auditors instill confidence in investors, lenders, and other stakeholders.

Enhancing Governance: Internal audits contribute to effective corporate governance by evaluating the organization’s governance framework, policies, and procedures. Auditors assess the effectiveness of oversight functions, including the board of directors and management committees, to ensure appropriate governance practices are in place. This promotes transparency, accountability, and ethical conduct within the organization.

Facilitating Continuous Improvement: Internal audits provide valuable insights and recommendations for improvement. By identifying areas of weakness or inefficiency, auditors help management implement changes that enhance operations, controls, and overall performance. Regular internal audits create a culture of continuous improvement, fostering innovation and adaptability within the organization.

VComply’s Internal Audit Management software streamlines and automates audit activities, procedures, and reporting.