Conflict of Interest Explained: What It Is When It Occurs, and How to Manage It

A conflict of interest occurs when personal interests or relationships interfere with professional responsibilities, potentially compromising objectivity and fairness. These conflicts can arise in both business and personal contexts, each bringing distinct challenges and implications. Recognizing and managing them is essential to maintain trust and ethical decision-making.

“It takes many good deeds to build a good reputation, and only one bad one to lose it.” – Benjamin Franklin.

Conflicts of interest (COIs) can undermine trust and tarnish an organization’s reputation, even when no wrongdoing occurs. Surveys across OECD countries reveal that while 66% have regulatory frameworks to address COIs, only a minority actively verify declarations or resolve conflicts in a timely manner, highlighting global enforcement challenges.

A conflict of interest arises when an individual’s personal interests, relationships, or activities compromise their ability to act in the organization’s best interests. Take, for example, an employee approving a contract with a vendor they have personal ties to. Even if the decision is fair, the perception of favoritism can erode trust and harm credibility.

So, how can organizations proactively identify and address COIs? This blog explores the issue in depth, providing practical insights on managing conflicts of interest to uphold ethical standards and maintain stakeholder trust.

Key Takeaways

- A conflict of interest arises when personal interests interfere with professional responsibilities.

- Conflicts can be personal (e.g., nepotism), corporate (e.g., undisclosed side projects), financial (e.g., insider trading), or professional (e.g., dual roles), each with unique implications.

- Even perceived conflicts, where no actual wrongdoing occurs, can erode trust and damage an organization’s reputation.

- Addressing COIs ensures decisions are based on merit and alignment with organizational goals.

- Effective COI management involves transparency, clear policies, recusal when necessary, and employee training, ensuring compliance and safeguarding ethical standards.

What Is a Conflict of Interest?

At its core, a conflict of interest arises when personal interests, relationships, or obligations clash with professional responsibilities, leading to a situation where impartiality and objectivity may be compromised.

With a deeper understanding, conflicts of interest can be categorized into business and personal contexts, each presenting unique challenges and implications.

Also Read: Identifying Ethical Challenges in Business: Bribery, Conflict of Interest, Honesty and Integrity

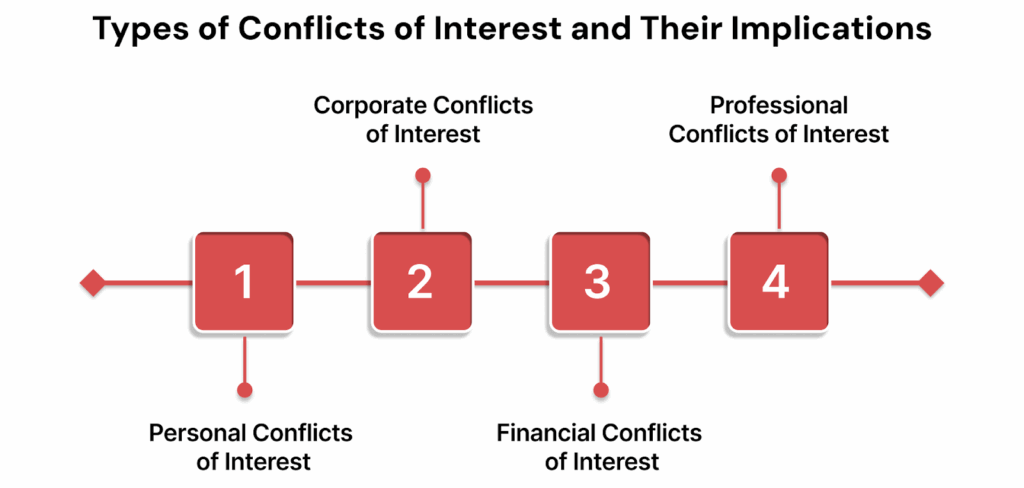

Types of Conflicts of Interest and Their Implications

Conflicts of interest can manifest in diverse ways, often overlapping across personal, corporate, financial, and professional domains. Addressing these conflicts requires a nuanced understanding of their specific nature and impact.

Additionally, distinctions between actual, potential, and perceived conflicts of interest provide further clarity on how to approach and resolve these issues effectively.

1. Personal Conflicts of Interest

Personal conflicts arise when relationships or personal interests interfere with an individual’s ability to make impartial decisions. These situations often involve conflicts of interest, which can create the appearance of favoritism or improper influence.

Examples:

- Nepotism: A manager hires a family member without disclosing the relationship.

- Undisclosed Relationships: An employee awards a contract to a vendor owned by a close friend.

- Favoritism: Assigning promotions based on personal connections rather than merit.

Personal conflicts can damage team morale, lead to accusations of unfairness, and undermine organizational ethics.

2. Corporate Conflicts of Interest

Corporate conflicts arise when an employee or decision-maker’s personal gain conflicts with the company’s objectives. These are often referred to as corporate conflicts of interest and can result in reputational harm and regulatory scrutiny.

Examples:

- Misaligned Priorities: A board member pushes for a merger with a company where they have investments.

- Undisclosed Side Projects: An executive is working part-time for a competitor without informing their employer.

Addressing these issues ensures alignment between individual actions and corporate goals, safeguarding organizational integrity.

3. Financial Conflicts of Interest

Financial conflicts occur when personal financial gain influences professional responsibilities, leading to ethical breaches or even legal consequences.

Examples:

- Insider Trading: Using confidential company information to buy or sell stocks for personal benefit.

- Kickbacks: Accepting personal rewards from a vendor in exchange for awarding a contract.

Managing financial conflicts of interest is critical to maintaining regulatory compliance and organizational trust.

4. Professional Conflicts of Interest

Professional conflicts arise when individuals hold dual roles or affiliations that create competing priorities, compromising their objectivity.

Examples:

- Legal Professionals: A lawyer representing two opposing clients in a case.

- Board Memberships: A board member voting on a decision that benefits another organization to which they are affiliated.

Resolving professional conflicts requires clear boundaries and adherence to ethical guidelines to prevent compromised judgment.

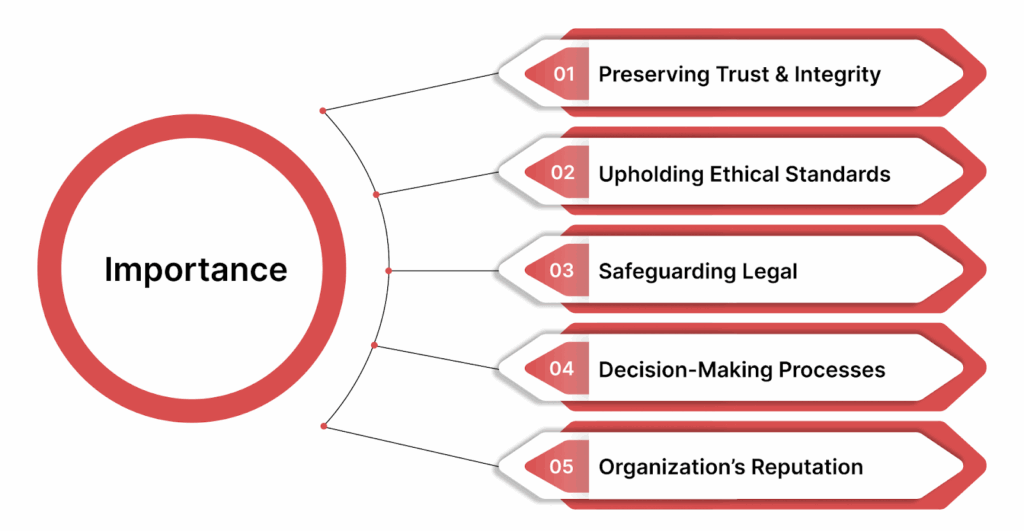

The Importance of Recognizing and Addressing Conflicts of Interest

Conflicts of interest, whether real or perceived, can have far-reaching consequences for any organization. Recognizing and addressing these conflicts early is crucial for maintaining a strong ethical foundation and protecting the organization’s reputation.

Here’s why it matters:

1. Preserving Trust and Integrity

At the heart of any successful organization lies trust. When employees or stakeholders perceive that decisions are influenced by personal interests, even if no wrongdoing occurs, trust begins to erode.

The perception of bias can be just as damaging as actual misconduct, leading to a breakdown in relationships and collaboration. By addressing COIs promptly, organizations can reassure their teams and clients that decisions are made fairly and without favoritism, reinforcing integrity across all levels.

2. Upholding Ethical Standards

Every organization has ethical guidelines that dictate how individuals should conduct themselves. Ignoring conflicts of interest undermines these standards, sending a message that ethical conduct is negotiable.

Proactively managing COIs helps ensure that the organization adheres to its values, setting a positive example for employees and stakeholders alike. It also creates a culture where ethical behavior is prioritized, encouraging a more transparent and accountable environment.

3. Safeguarding Legal and Regulatory Compliance

Failure to properly handle conflicts of interest can lead to legal issues, especially if it results in breaches of regulatory frameworks or industry standards.

As highlighted earlier, while many countries have regulatory frameworks addressing COIs, enforcement remains a challenge. By staying vigilant and adhering to compliance requirements, organizations can avoid the risk of legal repercussions, fines, or reputational damage.

4. Enhancing Decision-Making Processes

When conflicts of interest are left unchecked, they can distort decision-making processes. Whether in procurement, hiring, or contract approvals, COIs introduce bias that may compromise the quality of decisions.

Addressing conflicts ensures that decisions are based on merit, data, and the organization’s long-term goals, ultimately leading to better outcomes and more effective strategies.

5. Protecting the Organization’s Reputation

A single unresolved conflict of interest can spiral into a major crisis. News of COIs can spread quickly, damaging public perception and resulting in lost business, customer distrust, or even regulatory penalties.

By taking proactive steps to address COIs, organizations not only protect their internal culture but also safeguard their reputation in the eyes of the public, clients, and industry peers.

Also Read: Understanding the Importance and Implementation of a Business Code of Conduct

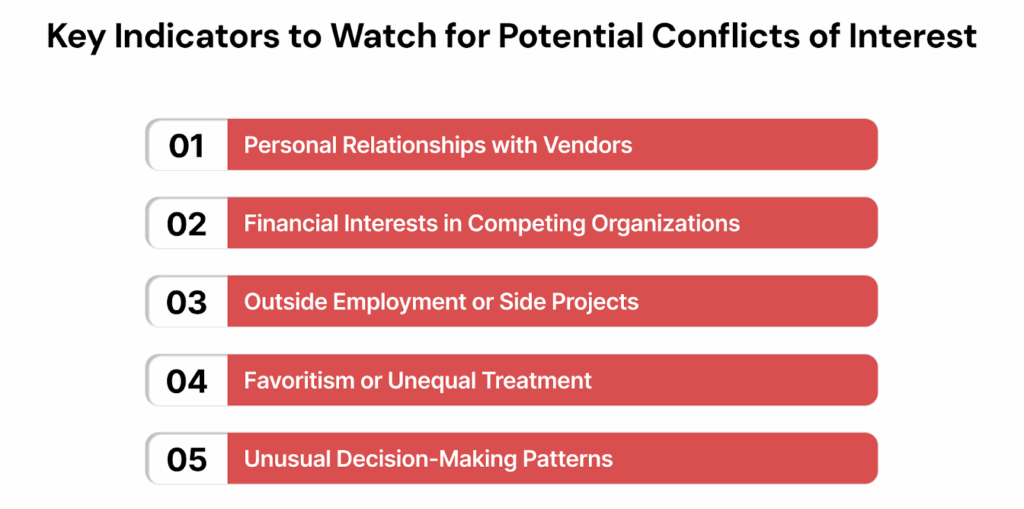

Key Indicators to Watch for Potential Conflicts of Interest

Recognizing the signs of potential conflicts of interest is essential for addressing them before they escalate into ethical or legal issues.

Below are key indicators that suggest a conflict may exist:

1. Personal Relationships with Vendors or Clients

- One of the most common red flags is when an employee has close personal or familial ties with a vendor, contractor, or client. While these relationships may be legitimate, they raise questions about impartiality when it comes to business decisions.

- If an employee is involved in approving contracts, negotiating terms, or making purchasing decisions for a vendor with whom they have a personal connection, it’s a potential conflict of interest.

2. Financial Interests in Competing Organizations

- Employees who hold financial stakes, such as stock or investment interests, in competing companies or organizations might be swayed in ways that aren’t aligned with their role.

- This financial interest can create a situation where their personal financial goals conflict with their responsibilities to the organization, leading to biased decision-making or a lack of objectivity.

3. Outside Employment or Side Projects

- When an employee works for or runs a side business that competes with their employer, it can create a direct conflict of interest.

- This is especially true if the employee uses insider information, resources, or time during work hours for their personal ventures.

- It’s essential to assess whether any external work or side project could compromise the employee’s loyalty and decision-making within the organization.

4. Favoritism or Unequal Treatment

- If an employee is showing favoritism towards a specific individual, department, or group, it can be a sign of an underlying conflict of interest.

- This behavior may manifest as biased decision-making, unequal distribution of opportunities, or preferential treatment in promotions or pay raises.

- Such actions can undermine morale and create an unhealthy work environment, which may escalate into more significant conflicts if not addressed.

5. Unusual Decision-Making Patterns

- If decisions are consistently made that benefit a particular individual or group without clear, justifiable reasons, it could indicate a hidden conflict of interest.

- For instance, awarding contracts or approving deals that disproportionately benefit one party or seem to go against the organization’s best interests might be a sign that a conflict is influencing decision-making.

Proactively addressing these signs ensures that potential conflicts are managed before they damage trust, disrupt operations, or lead to reputational harm. Regular audits, clear policies, and open communication are key tools for identifying and mitigating conflicts early.

How to Investigate Conflicts of Interest?

Figuring out conflicts of interest isn’t just about solving problems; it’s about making sure everyone stays on the same page.

Here’s how to tackle it effectively without overcomplicating things:

- Define the Issue: Begin with a precise determination of the nature and scope of the suspected conflict, identifying all parties involved, the interests at stake, and the decision-making processes that may be affected. Establishing clarity at the outset is essential for subsequent inquiry.

- Gather Relevant Evidence: Conduct a discreet and methodical collection of all pertinent documentation, such as emails, contracts, and meeting transcripts, to ensure a comprehensive understanding while minimizing disruption to normal operations.

- Conduct Objective Interviews: Hold structured interviews with relevant personnel, approaching each conversation with neutrality and professionalism. Ask direct questions and listen attentively, seeking to uncover facts rather than opinions or assumptions.

- Review Applicable Policies and Standards: Cross-reference the findings from interviews and documents with organizational policies and industry standards to determine whether any breaches or inconsistencies have occurred, focusing on both regulatory and ethical dimensions.

- Rely on Factual Evidence: Resist conjecture by maintaining strict adherence to verifiable facts. Assess only what is evidenced as influencing decisions or outcomes, avoiding assumptions that lack substantive support.

- Seek Independent Assessment: For sensitive or high-impact cases, bring in a neutral third-party expert to review evidence and validate conclusions. Independent oversight helps ensure the impartiality and credibility of the process.

- Implement Remedial Measures Promptly: When a conflict of interest is substantiated, execute appropriate corrective actions, such as reassigning duties, terminating conflicting agreements, or instituting additional safeguards—to prevent recurrence and preserve integrity.

By following these steps, you can effectively and ethically address conflicts within your organization. Next, let’s look at some practical tips for managing these conflicts.

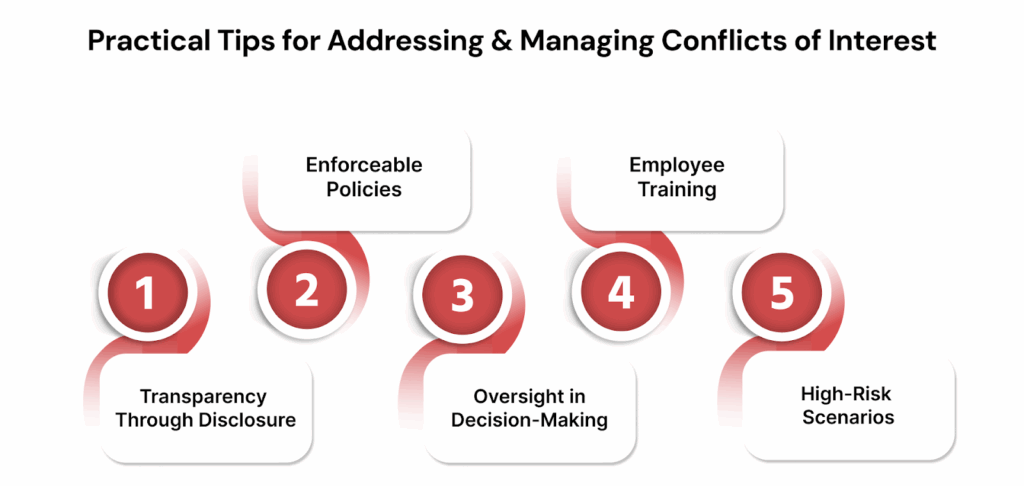

Practical Tips for Addressing and Managing Conflicts of Interest

Effectively managing conflicts of interest requires clear guidelines, transparency, and a proactive approach. These actionable tips help organizations and individuals manage conflicts in an ethical and efficient manner.

Here are the practical tips for addressing and managing conflicts of interest.

1. Transparency Through Disclosure

Openly declaring personal or financial interests that might influence decisions is essential to maintaining trust.

- Mandatory Disclosure Policies: Implement policies requiring employees to report relationships or financial ties during key processes like procurement and hiring.

- Foster a Culture of Transparency: Encourage employees to disclose potential conflicts of interest as a standard practice, promoting accountability and trust. Create an environment where proactive declarations are viewed as a positive step toward maintaining ethical standards.

2. Clear and Enforceable Policies

Well-documented, specific guidelines help prevent ambiguities that can lead to lapses in judgment.

- Define Scenarios: Clearly outline what constitutes a conflict of interest in business and professional contexts.

- Set Rules: Include limits on accepting gifts, engaging in dual employment, or handling personal relationships.

- Update Regularly: Revise policies to address emerging risks, like remote work dynamics or new regulatory requirements.

3. Recusal and Oversight in Decision-Making

When conflicts are unavoidable, stepping aside ensures impartiality.

- Recusal: Individuals should abstain from participating in decisions where they have a vested interest.

- Third-Party Oversight: Use independent committees or auditors to ensure transparency in high-risk situations.

4. Employee Training and Awareness

Knowledge is key to identifying and effectively managing conflicts.

- Interactive Training: Provide workshops and simulations to help employees recognize actual conflicts of interest and learn resolution strategies.

- Tailored Modules: Customize training for roles such as HR or procurement, focusing on scenarios relevant to their responsibilities.

- Continuous Education: Offer refresher courses to keep employees updated on policies and new risks.

5. Ethical Safeguards for High-Risk Scenarios

For complex or high-stakes conflicts, additional safeguards are critical.

- Ethics Screens: Restrict access to sensitive information for individuals with potential conflicts of interest.

- Blind Trusts: Manage financial interests without the individual’s direct oversight.

By creating transparency and implementing clear policies, organizations can establish a strong ethical foundation for sustained success.

Real-World Example of Conflict of Interest

One well-documented real-world example of a conflict of interest occurred in the case of Wells Fargo, a major American bank and financial services company. In the mid-2010s, Wells Fargo employees were found to have created millions of unauthorized bank and credit card accounts to meet aggressive sales targets.

The conflict of interest arose because employees were incentivized through remuneration and bonuses to push sales, leading some to prioritize personal and corporate sales goals over ethical banking practices and customer interests.

This case highlights how financial incentives can create conflicting loyalties between an employee’s duty to customers and their desire to meet performance goals.

The scandal severely damaged Wells Fargo’s reputation and led to regulatory actions, including a $3 billion settlement with the U.S. Department of Justice and the Consumer Financial Protection Bureau in 2020.

This example illustrates the dangers of unmanaged conflicts of interest where personal or organizational gain comes at the expense of ethical standards and stakeholder trust.

Simplify Conflict of Interest Management with VComply

VComply streamlines conflict of interest management in 2025 with specialized PolicyOps features, enabling organizations to draft, approve, distribute, and track policies on conflicts of interest across teams more easily.

How PolicyOps streamlines conflict of interest management:

- Centralized Policy Creation: PolicyOps enables organizations to standardize conflict of interest policies using AI-powered templates designed for regulatory consistency.

- Automated Workflows: The platform automates critical stages, drafting, review, approval, and distribution, so every stakeholder receives up-to-date conflict of interest policies promptly.

- Disclosure and Attestation Tracking: PolicyOps supports real-time monitoring of employee disclosures, annual declarations, and attestations tied to policies. It automates reminders for required conflict declarations during onboarding, procurement, or other high-risk periods.

- Compliance Audit Trails: Every policy update, disclosure, and acknowledgment is logged, producing strong audit trails. This assures readiness for compliance checks or internal reviews and supports a defensible record of conflict resolution efforts.

- Training and Communication: VComply’s PolicyOps offers integrated tools for policy-linked training and employee communication. Interactive modules ensure everyone understands their conflict of interest obligations and how to report concerns transparently.

Use VComply’s Conflict of Interest Policy Management Template to create and share clear, consistent policies. This ready-to-use template streamlines communication, establishes clear expectations, and makes your guidelines easily accessible throughout your organization.

Start your Free Demo with VComply today! Take the first step toward a more streamlined and accountable workplace.

Final Thoughts

If left unaddressed, conflicts of interest can erode trust, disrupt decision-making, and tarnish reputations. Understanding the various types of actual, potential, and perceived conflicts of interest is the first step in creating a culture of integrity and accountability.

Organizations that prioritize addressing conflicts of interest are better positioned to maintain ethical standards, safeguard their reputations, and build trust with stakeholders.

Equip your organization with the right tools to effectively manage conflicts of interest, ensure compliance, and promote transparency. Explore VComply’s 21-day free trial today and take the first step toward building a more ethical and accountable workplace.

FAQs

Employees should proactively disclose any personal, financial, or professional interests that could influence their decisions, typically through formal disclosure forms and company policies.

Management includes transparent disclosure, recusal from conflicted decisions, clear policies, employee training, oversight mechanisms, and regular audits to detect and mitigate conflicts early.

Yes, even perceived conflicts can erode trust, cause reputational damage, and disrupt workplace harmony, so it’s crucial to address perceptions as well as actual conflicts.

A policy ensures clarity on what constitutes a conflict, sets expectations for disclosure and behavior, provides procedures for managing issues, and helps protect the organization legally and ethically.

Organizations can promote transparency by encouraging open communication, providing regular training on ethical practices, and establishing safe channels for reporting concerns. This encourages a culture where employees feel comfortable disclosing potential conflicts without fear of retaliation.