What Are the Types of Audit Evidence? How Do You Collect Them?

Audit evidence refers to the information and documentation that auditors gather and use to support their findings and conclusions during an audit process. It provides the basis for auditors to form an opinion on the accuracy, checks if the company is following regulations, and examines the sanctity of the organization’s compliance posture, financial statements, and assertions.

An audit, in its essence, is a journey to uncover the truth within financial statements. Audit evidence is the compass that guides auditors through this journey, ensuring they reach accurate and reliable conclusions. This evidence is not just paramount; it’s the bedrock upon which stakeholders build their trust in the financial statements they rely on.

According to the American Institute of Certified Public Accountants (AICPA) standards, audit evidence consists of all the information used by the auditor to arrive at their conclusions. This includes both the underlying accounting records and other corroborating information from various sources, as it plays a crucial role in forming auditors’ conclusions and opinions.

In this blog, we will delve into the various types of audit evidence and the meticulous process of collecting them, highlighting their critical role in maintaining the integrity of financial reporting. So, let’s start by understanding what audit evidence actually is and why it’s so central to the audit process.

Key Takeaways (TL;DR)

-

Understand what audit evidence is and why it’s crucial for accurate and reliable financial reporting.

-

Explore the types of audit evidence, including documentary, observational, external, digital, and expert opinion evidence.

-

Learn systematic approaches for collecting audit evidence while adhering to auditing standards and regulatory guidelines.

-

Discover methods for evaluating audit evidence for sufficiency, appropriateness, reliability, and completeness.

-

Stay updated on emerging audit trends like AI, blockchain, ESG reporting, and cybersecurity auditing for modern audit challenges.

What is Audit Evidence and Its Importance?

Audit evidence refers to the information collected by auditors to support their conclusions and opinions on an entity’s financial statements. It includes a variety of data, such as documents, records, and observations, that auditors use to ensure the accuracy and completeness of financial reports. Sufficient, relevant, and reliable evidence is essential for a credible audit process.

Importance of Audit Evidence

Audit evidence is crucial for supporting auditors’ opinions and ensuring the accuracy of financial statements. Here’s why it is important:

- Cornerstone for Assessing Compliance: Audit evidence serves as the foundation for assessing compliance with regulatory requirements and ensuring the reliability of financial statements. It helps auditors verify that the entity follows applicable laws and standards.

- Essential for Independent Opinions: Auditors require evidence to express independent opinions on the financial condition of the entity. It provides the factual basis needed to form unbiased and accurate audit conclusions.

- Supports Risk Assessment: Evidence functions in risk assessment, helping auditors identify areas of potential risk and determine the scope and nature of their audit procedures. It supports the overall audit opinion by ensuring that all significant risks are adequately addressed.

Now that we know why it’s important, let’s dive into the different types of audit evidence auditors rely on.

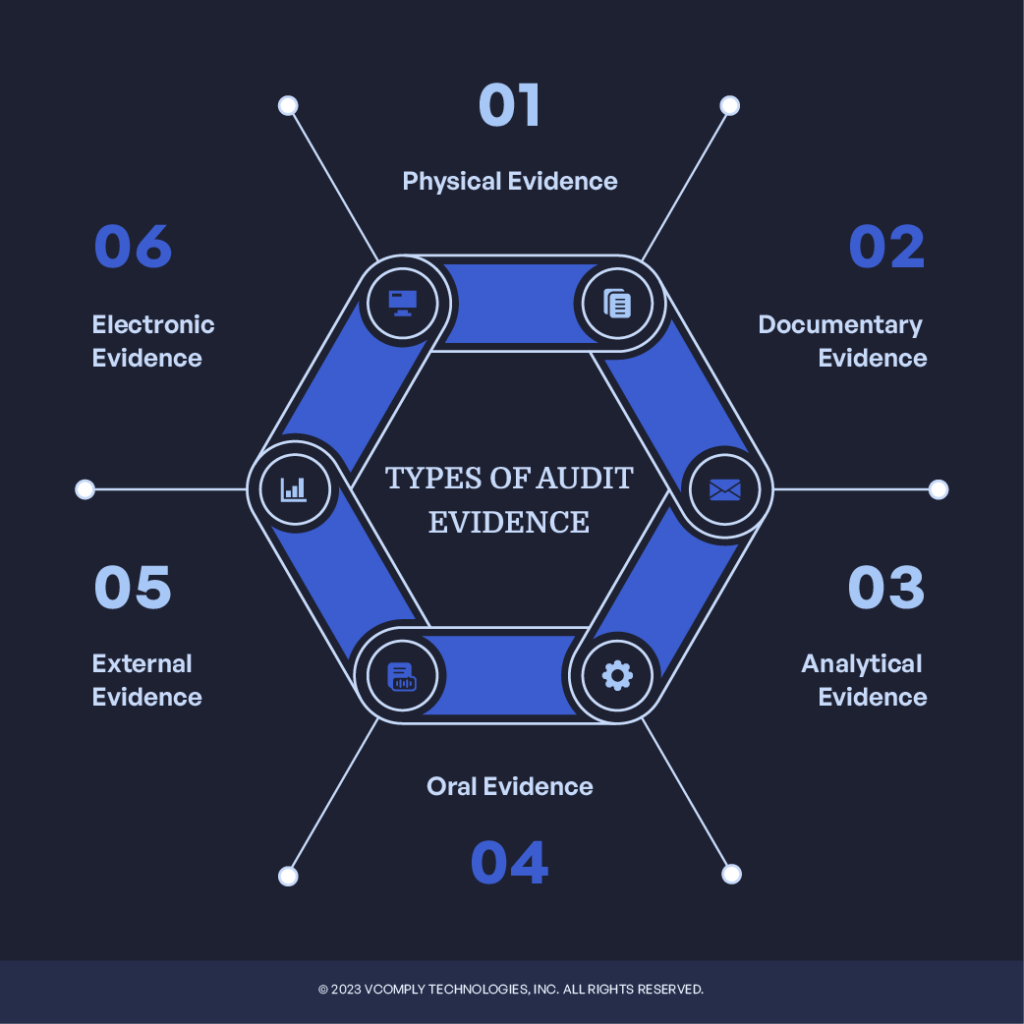

Types of Audit Evidence

Audit evidence comes in various forms, each serving a unique purpose in the auditing process. The diverse types of evidence collected provide a comprehensive view of an entity’s financial health and compliance status.

Let’s explore the different types of audit evidence. First up, let’s take a look at documentary evidence and why it’s essential.

Documentary Evidence

Documentary evidence includes written records like invoices and legal documents that substantiate the transactions and operations of an entity. These documents are essential for verifying the accuracy of financial statements and ensuring adherence to regulatory requirements.

- Invoices: Provide proof of sales and purchases, showing details of transactions and helping to verify revenue and expenses.

- Contracts: Outline the terms and agreements between parties, ensuring that transactions are legally binding and accurately recorded.

- Bank Statements: Offer a detailed account of financial transactions, helping to reconcile the entity’s records with actual bank balances.

- Receipts: Serve as evidence of payments made and received, supporting the recorded expenses and revenues.

- Legal Documents: Include deeds, titles, and other legal paperwork that confirm ownership and contractual obligations.

- Purchase Orders: Confirm the details and authorization of purchases, ensuring that procurement procedures are followed correctly.

- Shipping and Delivery Documents: Provide evidence of goods being shipped and received, verifying inventory levels and purchase transactions.

- Internal Reports: Internal audit reports and compliance reports provide preliminary insights into internal controls and adherence to policies, which auditors then evaluate further.

Analytical Evidence

Auditors use analytical procedures involving analytical evidence to evaluate financial information. These procedures help auditors identify trends, anomalies, and relationships that might indicate potential issues or areas requiring further investigation.

- Ratio Analysis: This involves calculating financial ratios (e.g., liquidity, profitability, and solvency ratios) to assess the entity’s financial health. It helps auditors compare performance across periods or against industry benchmarks.

- Trend Analysis: Examines changes in financial statement items over time to identify patterns and significant deviations. It aids in understanding the entity’s financial trajectory and pinpointing unusual fluctuations.

- Comparative Analysis: Compares financial data with prior periods, budgets, or forecasts to detect inconsistencies. It assists auditors in identifying discrepancies that warrant further scrutiny.

- Variance Analysis: Analyzes differences between actual and expected performance, often used in budgeting and forecasting. It helps auditors understand the reasons behind variances and their implications.

- Reasonableness Tests: Involves evaluating the reasonableness of financial data based on known relationships and expectations. This technique is used to identify figures that do not align with typical patterns or standards.

Next, let’s move from numbers and analysis to what auditors can observe directly in organizations.

Observational Evidence

Observational evidence involves auditors directly observing assets, operations, and internal controls to verify their existence and functionality. This type of evidence provides first-hand insight into the entity’s processes and helps ensure that reported information accurately reflects reality.

- Physical Verification: Inspecting tangible assets such as inventory, equipment, and property to confirm their existence and condition.

- Observation of Processes: Watching employees perform specific tasks to assess the effectiveness of internal controls.

- Walkthroughs: Tracing a transaction from initiation through the entire accounting cycle to verify the effectiveness of controls at each stage.

- Inspection of Facilities: Touring company facilities to understand operational processes and physical security measures.

Looking beyond internal observations, let’s explore the types of evidence auditors can obtain from external sources.

External Evidence

External evidence obtained from third-party sources often provides a more independent perspective; however, auditors must still evaluate it for relevance and reliability. This type of evidence is considered highly reliable due to its unbiased nature.

- Confirmation Letters: Sent to external parties like banks, customers, or suppliers to verify account balances and transactions. These letters confirm the accuracy of financial records by cross-referencing them with independent third-party data.

- Third-Party Statements: Includes bank statements, vendor invoices, and legal confirmations. These documents provide independent verification of transactions and balances reported by the entity, ensuring accuracy and compliance.

- External Audit Reports: Reports from external auditors or regulatory bodies offer an objective assessment of the entity’s financial statements and compliance status, adding an extra layer of credibility to the audit.

- Market Data: Information from external market sources, such as stock prices, market trends, and industry benchmarks. This data helps in assessing the entity’s performance in relation to market and industry standards, providing context for the financial statements.

- Credit Reports: Information obtained from credit reporting agencies evaluates the creditworthiness and financial stability of the entity, offering insights into its financial health from an external perspective.

Electronic and Digital Evidence

Electronic and digital evidence includes information stored electronically, such as emails and digital records. This type of evidence provides comprehensive data that can be easily accessed and analyzed.

- Emails: Provide a record of communication between parties, offering insights into transactions and decision-making processes. Helps verify the authenticity and context of business communications and agreements.

- Digital Records: Includes electronic documents, spreadsheets, and databases that contain financial and operational data. Allows for efficient verification and analysis of large volumes of data.

- Audit Logs: Digital logs that track system activities and user actions. Assists in monitoring compliance and detecting unauthorized access or fraudulent activities.

- Electronic Invoices and Receipts: Digital versions of traditional invoices and receipts. Ensures accurate and organized record-keeping of financial transactions.

- Cloud Storage Records: Data stored on cloud platforms, including backup files and archives. Provides a secure and accessible means of storing and retrieving critical financial information.

- Digital Signatures: Electronic signatures are used to validate the authenticity of documents. Ensures the integrity and non-repudiation of agreements and transactions.

- System Access Records: Logs detailing who accessed what information and when. Helps track user activities and ensures data integrity and security.

Physical and Oral Evidence

Physical and oral evidence involve direct interactions and observations that provide auditors with firsthand information about the entity’s operations and controls. These types of evidence offer practical insights that are crucial for verifying the accuracy of financial records and assessing internal controls.

- Physical Inspections: Involves examining tangible assets like inventory, equipment, and property. This helps verify their existence, condition, and proper valuation.

- Verbal Interviews: Conducting interviews with employees and management to gather insights on processes and controls. This aids in understanding the effectiveness of internal controls and identifying potential issues.

- Observation of Procedures: Watching the execution of specific tasks or processes ensures that the procedures are being followed correctly and consistently.

- Facility Tours: Touring company facilities to observe operations and physical security measures. This provides a comprehensive view of the entity’s operational practices and safeguards.

- Meetings with Management: Regular meetings to discuss operational processes and internal controls. These discussions help to identify areas of improvement and potential risks.

- Employee Surveys: Distributing surveys to gather employees’ perspectives on internal controls and compliance issues. This helps to uncover potential problems and areas for improvement.

Re-performance and Expert Opinion Evidence

Auditors independently re-perform procedures and consult specialists to gain insights into complex issues involving re-performance and expert opinion evidence. These types of evidence provide a higher level of assurance regarding the accuracy and reliability of financial information.

- Re-performance of Procedures: Auditors independently execute procedures initially performed by the entity’s personnel to verify results. Ensures that processes are performed correctly and consistently, validating the accuracy of the entity’s records.

- Consulting Experts: Engaging specialists in fields such as legal, tax, or valuation to provide insights on complex matters. Provides expert opinions on specialized issues that require technical knowledge beyond the auditor’s expertise.

- Analytical Re-computation: Re-computing figures and calculations to verify the accuracy of financial data. Confirms the correctness of mathematical calculations in financial statements.

- Technical Reviews: In-depth reviews of specific technical areas, such as IT systems or environmental compliance, conducted by subject matter experts. Assesses the adequacy and effectiveness of technical processes and controls.

- Second Opinions: Seeking a second opinion from another auditor or specialist to validate complex or contentious issues. Ensures unbiased and thorough verification of critical aspects.

Collecting this diverse range of audit evidence requires a systematic and reliable approach, so let’s look into how auditors gather it effectively.

Collecting Audit Evidence

The systematic process of collecting evidence ensures the information gathered is reliable and sufficient to support audit conclusions. This involves adhering to established standards, implementing various audit procedures, and ensuring the evidence is appropriate and complete.

Adherence to Auditing Standards and Regulatory Guidelines

Adhering to auditing standards and regulatory guidelines ensures the integrity and credibility of the audit process. Auditors must follow established protocols to collect reliable and sufficient evidence. Here’s how you can do that.

- Understand Relevant Standards: Familiarize yourself with international standards like ISA and local regulatory requirements.

- Document Procedures: Clearly document all audit procedures and ensure they align with established standards.

- Continuous Training: Engage in regular training to stay updated on the latest auditing standards and regulations.

- Use Standardized Checklists: Employ checklists to ensure all necessary steps and requirements are met during evidence collection.

- Quality Control: Implement quality control measures to review and verify that all collected evidence complies with the required standards.

Implementation of Audit Procedures

Auditors use a systematic approach to gather and assess evidence by implementing audit procedures. Key procedures include the following.

- Risk Assessment Procedures: Identify and evaluate risks of material misstatement through understanding the entity and its environment.

- Substantive Procedures: Test for material misstatements in financial records through a detailed examination of transactions and balances.

- Compliance Procedures: Ensure the entity adheres to relevant laws and regulations by examining relevant documents and processes.

- Analytical Procedures: Evaluate financial information through ratio analysis, trend analysis, and other analytical techniques to identify any unusual or unexpected relationships.

Utilizing a Mix of Audit Procedures

Incorporating a diverse range of audit procedures ensures a thorough and effective audit. Each type of evidence provides unique insights and helps address different aspects of the audit. Here’s how to blend these procedures to meet various audit objectives:

- Inspection of Records and Documents: Review documentary evidence such as invoices, contracts, and bank statements. This helps verify the accuracy of recorded transactions and financial positions.

- Analytical Procedures: Employ ratio and trend analysis to identify anomalies in financial data. By comparing financial ratios and trends over time or against industry benchmarks, auditors can detect irregularities.

- Observation: Conduct direct observation of assets and internal controls. This includes visiting physical locations to inspect assets and observe control processes in action, ensuring they are functioning as intended.

- External Confirmations: Obtain information from third-party sources like bank confirmations and vendor statements. This provides an independent perspective, corroborating the information provided by the entity.

- Recalculation and Reperformance: Independently execute procedures initially performed by the entity’s personnel to verify results. This includes recalculating figures and re-performing processes to ensure accuracy.

- Inquiry and Interviews: Engage in verbal interviews with employees and management to gather insights on processes and controls. This helps understand the effectiveness of internal controls and identify potential issues.

- Inspection of Tangible Assets: Physically inspect tangible assets and facilities. This confirms their existence and condition, supporting the values recorded in financial statements.

Leveraging advanced audit management tools like VComply can enhance the efficiency and effectiveness of the audit process. It offers features that facilitate efficient audit planning, execution, and reporting, ensuring that all audit procedures are thoroughly and effectively implemented.

Once the evidence is collected, the next critical step is evaluating it—let’s see how that’s done.

Evaluation of Audit Evidence

Auditors evaluate audit evidence, ensuring that the collected data is sufficient, appropriate, and reliable for forming audit conclusions. Through careful evaluation, auditors can confidently base their opinions on solid and credible evidence, enhancing the overall integrity of the audit.

Assessing the Collected Evidence

Auditors assess the collected evidence to ensure that audit conclusions are reliable and credible. This step involves a careful examination of the sufficiency, appropriateness, and completeness of collected evidence. Here’s how you do it.

Sufficiency: Ensure that the volume of evidence is adequate to support audit conclusions.

- Cross-Verification: Use multiple sources to confirm the same information, enhancing the reliability of the evidence.

Appropriateness: Verify that the evidence is relevant and reliable.

- Relevance Check: Ensure the evidence directly relates to the audit objectives and the specific financial statement assertions being tested.

- Quality Review: Assess the reliability of the evidence-based on its source, including the credibility and independence of third-party evidence.

Completeness: Confirm that all necessary evidence has been gathered.

- Gap Analysis: Identify and address any missing information or discrepancies in the evidence to ensure a comprehensive audit.

Evaluating the Reliability of Audit Evidence

Auditors evaluate the reliability of evidence to ensure that they base the conclusions on credible and dependable information. Here’s how to evaluate the reliability of evidence.

- Source of Evidence: Determine the origin of the evidence to assess its credibility. Evidence from independent third parties (external) is generally more reliable, while internal evidence should be corroborated with other data due to potential bias.

- Auditor’s Independence: Ensure that the auditor maintains objectivity and impartiality by avoiding conflicts of interest and maintaining professional skepticism throughout the audit process.

- Nature of Evidence: Evaluate whether the evidence is internal or external. Evaluate if the internal evidence is consistent with the organization’s policies and procedures and whether it aligns with external evidence.

Special Considerations

Special considerations help to address unique challenges that require auditors to apply additional scrutiny and specific techniques to ensure the evidence is robust and reliable. It involves.

- Fraud Detection: Implement procedures to identify potential fraud, such as reviewing unusual transactions and conducting forensic accounting techniques.

- Ongoing Concern Issues: Assess whether the entity can continue operating for the foreseeable future by examining financial health indicators and management plans.

- Complex Transactions: Evaluate complex or unusual transactions in detail to understand their substance and ensure they are properly recorded.

- Related Party Transactions: Examine transactions between related parties to confirm they are conducted at arm’s length and properly disclosed.

Now, let’s explore the latest trends and challenges auditors face in today’s fast-evolving business landscape.

Emerging Trends and Challenges

The landscape of auditing is rapidly evolving, driven by technological advancements and new regulatory demands. Staying ahead of these changes is critical for maintaining audit effectiveness and relevance.

Adapting to Technological Advancements

Technologies like AI, blockchain, and continuous auditing have the potential to transform the audit process. AI can enhance data analysis, blockchain may provide secure and transparent transaction records, and continuous auditing could allow for real-time monitoring as these technologies mature.

ESG Reporting and Cybersecurity Auditing

Environmental, Social, and Governance (ESG) reporting and cybersecurity auditing are becoming increasingly important. Auditors must ensure comprehensive assessments of an entity’s sustainability practices and cyber risk management.

Common Challenges

Obtaining and evaluating audit evidence presents ongoing challenges, such as ensuring data accuracy, managing large volumes of information, and dealing with incomplete or biased data.

Leveraging advanced audit management tools like VComply can help address these challenges by providing a robust framework for efficient and effective auditing in the modern landscape.

Conclusion

Audit evidence is the cornerstone of a reliable and credible audit process. It encompasses various types, each crucial for different audit objectives. Proper evidence collection and evaluation are paramount in maintaining audit quality ensuring accurate and trustworthy financial statements. The dynamic nature of audit evidence necessitates that auditors continually adapt their strategies to cope with evolving challenges and technological advancements.

To streamline and enhance your audit processes, consider leveraging advanced tools like VComply. Its robust features support comprehensive audit management, making it easier to collect, evaluate, and manage audit evidence effectively.Ready to transform your audit approach? Request a demo of VComply today!